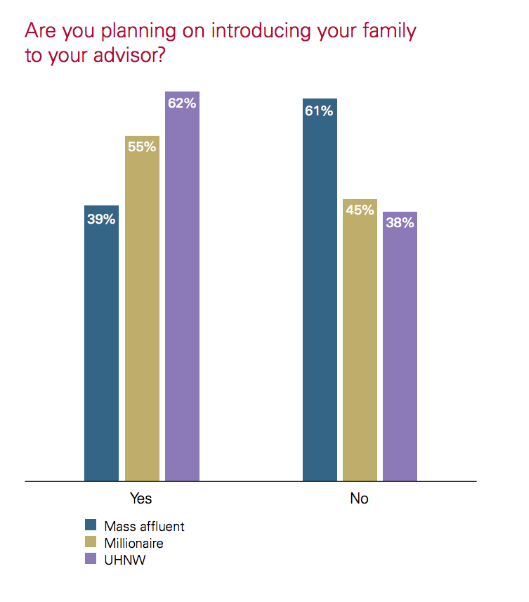

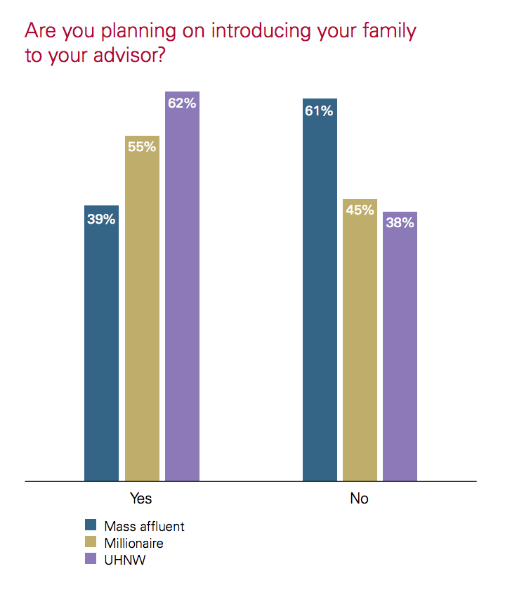

Are you ready for the great wealth transfer? As $30 trillion transfers from baby boomers to the next generations over the coming decades, many advisory firms fear seeing their managed assets slip from their grasp as clients’ beneficiaries take their money elsewhere. Here are the facts: 66% of children fire their parents’ financial advisors after receiving an inheritance. On average, only 50% of the wealthy intend to introduce their family to their advisor. Only 20% of advisors are targeting family members of clients.

The top reason advisors can’t retain clients’ assets passed to heirs is lack of a relationship.

Even advisors who believe their personal and professional relationships with clients couldn’t be stronger are likely leaving relationships untapped and assets on the table. Specifically, most advisors are failing to seize the opportunity to develop a solid relationship with their clients’ beneficiaries.

Given the enormous quantity of assets at stake in this impending transfer, no amount of preparation is unwarranted. Fortunately, there are solutions requiring very little time and effort. You don’t need to offer perks or host events to cultivate extended networks. Nor must you set up quarterly meetings with every family member. Rather, simple, sustained communication and relationship-building with the next generation of clients is all that is needed.

A 2013 study found that by getting to know your clients’ beneficiaries before a major event occurs, you’re more likely to retain assets under management. More often than not, recipients of an inheritance leave assets with their benefactor’s advisor for about a year. In that time, if no counsel is offered and no meaningful relationship is established, the inheritors take their assets to the first wealth advisor who fills this need. The authors of the study recommend beginning relationships now so that you’re already a trusted figure through difficult times.

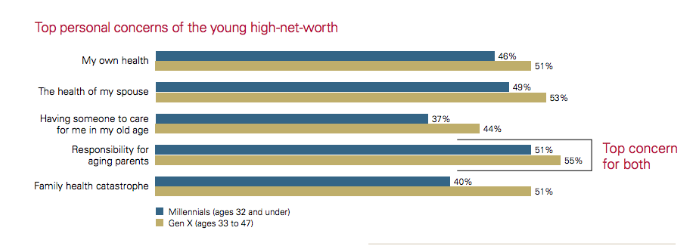

Younger investors are looking for more direction and have questions about the future, but many don’t have financial advisors or they use robo-advisors instead. Of primary concern is the responsibility they feel for the well-being of their aging parents. This is an excellent opportunity to spark a lasting relationship with your clients’ children. Involving them in life planning discussions will alleviate uncertainties and establish yourself as a knowledgeable, trusted figure.

Additionally, advisors are hesitant to engage a generation that prefers digital relationships to the traditional methods of interaction preferred by their parents. Advisors who have spent years relying on in-person meetings and phone calls don’t know how best to bridge the communication gap with millennials and Gen Xers. However, the solution is quite simple: place your expertise and services in front of them where they are – email and social media – and do so consistently.

Using Digital Communication to Meet Clients’ Beneficiaries

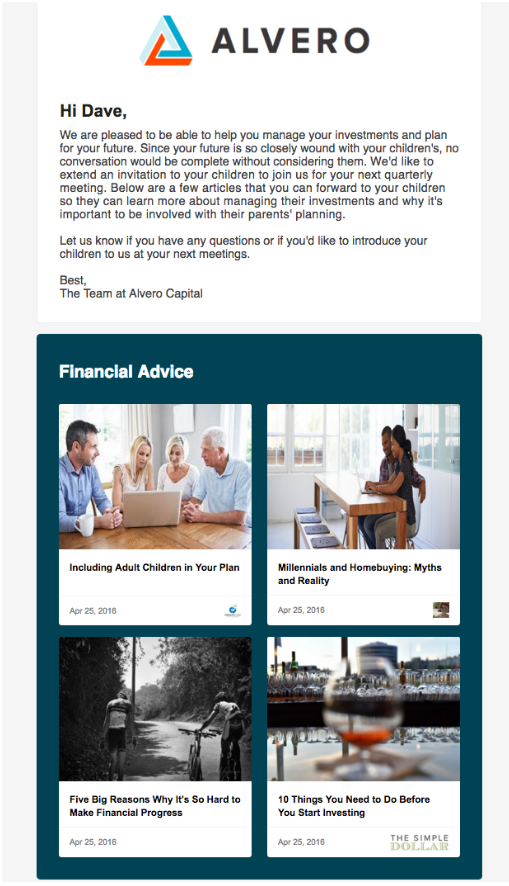

Below is an example of a simple email that could be used to initiate a relationship with beneficiaries. It indicates to your clients the importance of involving their adult children in planning, it offers something educational to those children, and it establishes a digital connection between you and their beneficiaries.

Phil Henry, Henry Wealth Management

Phil Henry, Henry Wealth Management

Phil Henry of Henry Wealth Management uses his digital communication to meet the next generation where they already are – online. Phil spent 30 years acquiring clients the old fashioned way – by meeting people, spending time with them, and developing lasting relationships. He took the time to get to know every one of his clients. But, now that he’s secure with his older clients, he wants to cultivate similar lasting relationships with their children too.

He thinks of digital communication as the beginning to real relationships. “Now at the end of the day you still have to look somebody in the eye, shake their hand, and build trust. If you can get in front of more people and motivate them to meet with you through an initial electronic meet, that’s more catered to a young person. That’s how they want to do it.”

Henry’s client's beneficiaries don’t have financial advisors because they don’t have the means yet or they haven’t seen a need. But these beneficiaries will have the means someday and they’ll have college friends and less qualified acquaintances who also want to give advice and build up their own AUM. To maintain relationships, Henry says, “They’re on my newsletter list. And they’re getting my communication. And we’re building a relationship, even though I don’t hang out with them. If I do that, when that lump inheritance comes in, there’s a much bigger chance they’ll stay with me.”

If you can turn your client's beneficiaries into loyal consumers of your content by becoming a valued information resource for them online, you’ll find that a real-world relationship naturally follows.

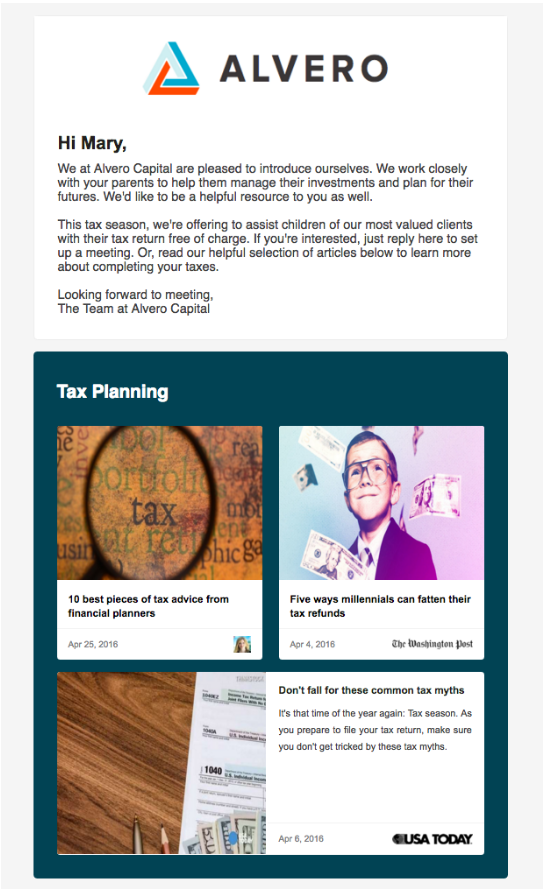

Below is an example of communication that could be sent directly to your clients’ beneficiaries to initiate a direct relationship.

Many advisors who work exclusively with baby boomers are hesitant to embrace digital communications because they know their clients don’t have social media accounts and ignore incoming emails. It may be the case that some of your clients aren’t proactively looking for valuable content online, but you can be sure that their children are. You may be missing a valuable opportunity to position yourself as a visible, informed figure who leverages the most cutting-edge digital technology to serve personalized insights to current and future clients.

Absent forethought and timely preparation, it is more likely than not that your clients’ assets will not remain under your firm’s management in the coming years and decades. The opportunity to advise the next generation of wealth management clients is well within your grasp with the right technology.

Henry Wealth Management and other advisors use Vestorly to curate the content that their audiences finds most engaging on a consistent basis via email, social media, and the web.

-----

This post was authored by Anna Huston and originally appeared on the Vestorly blog.